Putting the 2Q GDP decline and stock market performance in perspective

Remember back in late May when the Commerce Department reported that our U.S. economy shrank by 5% in the first quarter of 2020? And since that time economists were predicting that the second quarter of 2020 would be even worse?

Well, on Thursday, July 30th, the Commerce Department reported that GDP decreased at an annual rate of 32.9% in the second quarter of 2020. It was the worst quarterly decline in history.

Was Anyone Really Surprised?

The data from the BEA’s GDP report includes a wealth of information, including details on how much we spend and on what, inflation indices, corporate profits and details on imports and exports. So given the timeline of COVID-19 shutdowns in the U.S., why is the drop in the first and second quarter so surprising?

Yes, both drops are historic and difficult to fathom, but let’s remember a few things and try to keep a longer-term perspective.

A few things investors should remember:

- On January 21st, the U.S. announced its first known case of coronavirus in Washington State

- On January 23rd, China placed Wuhan, a city with about 11 million people, under quarantine. It should be noted that if Wuhan was in the U.S. it would be the largest city in our country by a long shot, roughly the same population as New York City (#1 at 8.3 million) and Los Angeles (#2 at 3.9 million)

- On January 31st, President Trump halted entry into the U.S. to those who had recently visited China and soon thereafter American Airlines, Delta and United Airlines suspended service between the U.S. and China. The suspension sent the stock market into worry-mode as Wall Street tried to predict the impact such a move would have on the world’s two largest countries and the effect on a global supply chain that relies so heavily on China. Unsurprisingly, the stock markets had one of their worst days then, falling close to 2%

- On February 28th, the U.S. recorded its first death from the coronavirus – a man from Washington state

- In early March, large-scale events started cancelling, beginning with Austin, Texas cancelling the South by Southwest conference

- By mid-March, the NBA, MLB, NHL and the NCAA begin cancelling seasons

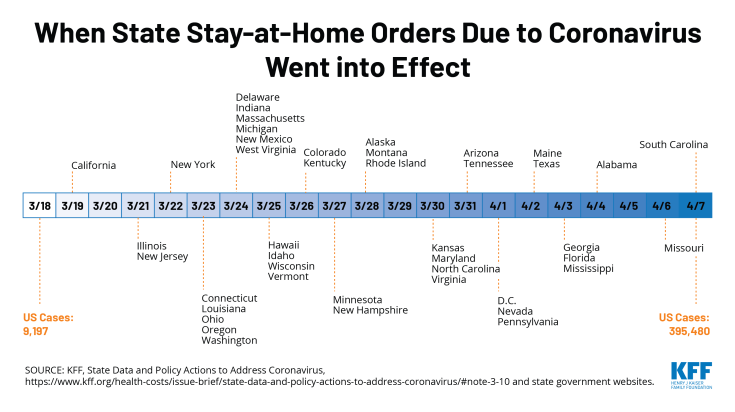

- Also in mid-March, states started issuing stay-at-home orders, beginning with California, home to 40 million Americans and followed a few days later by Illinois, New Jersey, New York, Ohio, and Michigan, home to another 63 million. That’s about 1/3 of the country. By the first week in April, 43 states had issued stay-at-home orders.

Given all that activity, is it surprising at all that our economy shrunk by 5% from the period January 1st through March 31st?

Understanding GDP Data

The Commerce Department’s Bureau of Economic Analysis compiles the GDP report monthly and it is one of the most closely-watched reports on our economy given how much economic information it contains. Not only does the GDP report provide detailed data on how our economy is performing, but it also provides data that can help investors identify certain trends going forward.

Broadly speaking, there are four main components of the GDP report, including:

- Personal consumption;

- Business investment;

- Government spending; and

- Net exports.

As such, the media and investors pay attention to GDP numbers because the data paints a very good picture of the economic backdrop for both equity and fixed-income markets alike, which of course helps inform the performance of stock and bond markets.

Why GDP Plummeted

Unless you’ve been living under a rock, you know the reason behind the drop in our GDP: COVID-19. In fact, this is taken directly from the GDP release:

“The decline in second quarter GDP reflected the response to COVID-19, as “stay-at-home” orders issued in March and April were partially lifted in some areas of the country in May and June, and government pandemic assistance payments were distributed to households and businesses. This led to rapid shifts in activity, as businesses and schools continued remote work and consumers and businesses canceled, restricted, or redirected their spending. The full economic effects of the COVID-19 pandemic cannot be quantified in the GDP estimate for the second quarter of 2020 because the impacts are generally embedded in source data and cannot be separately identified.”

But Perspective is Important

Yes, the second quarter GDP decline of almost 33% was the worst on record and dwarfs the previous record. But those with a glass-half full perspective will keep in mind that this was for the second quarter only, not the entire year.

In fact, given the gradual reopenings in the U.S. and around the world, expectations for GDP numbers in the third quarter of 2020 are expected to be historic too – historically positive.

For example:

- The GDPNow model is published by the Federal Reserve Bank of Atlanta (which they are quick to point out is not an official forecast of the Atlanta Fed or a forecasting model). As of July 31st – and of course a lot can change – the GDPNow model estimate for real GDP growth (seasonally adjusted annual rate) in the third quarter of 2020 will be 11.9%;

- The New York Fed publishes its NowCast, a similar index to the GDPNow model published by the Atlanta Fed. As of July 31st, the NowCast model estimates that third quarter GDP growth will be 16.9%;

- The Congressional Budget Office is predicting that GDP will rise at an annual rate of 21.5% for the third quarter;

- The current Blue Chip consensus forecast for the third quarter is 17.7%

Let’s assume GDP for the third quarter is somewhere north of the Atlanta and New York Feds’ estimates but below the CBO’s estimate – say 20%. Should investors get overly excited if the third-quarter GDP number comes in at 20%? Because after all, that would be the highest GDP gain of all time (previous record was about 16%).

The answer is no.

Focusing on the Positive

Again, the number everyone focused on from the Commerce Department was the 32.9% decline in GDP. But buried further in the news release was some positive data, including that:

- Current-dollar personal income increased $1.39 trillion in the second quarter

- Disposable personal income increased $1.53 trillion, or 42.1%, in the second quarter

- Real disposable personal income increased 44.9%

- Personal outlays decreased $1.57 trillion

- The personal saving rate – personal saving as a percentage of disposable personal income – was 25.7% in the second quarter, compared with 9.5% in the first quarter

More Perspective

The Council of Economic Advisers, an agency within the Executive Office of the President, released a few economic data points and conclusions on the same day GDP numbers were released, including the statement that:

“The U.S. economy entered this contraction on a healthier and more resilient footing than it did both prior to the Financial Crisis of 2008-09 and relative to other advanced economies.”

In support of that statement, the Council of Economic Advisers furthers states that:

- Household liabilities as a percent of personal disposable income were 136 percent leading into the Financial Crisis but were below 100 percent prior to this pandemic

- The United States had the highest growth rate among the G7 countries prior to the pandemic, with growth roughly double the non-U.S. G7 average from when President Trump took office through to the end of 2019

- The record-breaking number of jobs added in both May and June beat market expectations by a combined 11.7 million

- Data indicates that 80% of America’s small businesses are now open, up from a low in April of just 52%

And Last but Not Least, Remember the Markets Look Forward, Not Backward

It can be challenging to reconcile why stock markets could conceivably perform well amidst a constant barrage of negative economic news. Intuitively, it just doesn’t make sense. But the apparent disconnect between markets and the economy is actually normal.

Need an example? Consider that on the same week investors were digesting the massive 33% quarterly GDP drop, the S&P 500 quietly moved into positive territory for the year. And while the concentrated, 30-stock DJIA is still in the red for the year, NASDAQ is up almost 20% – and NASDAQ tracks more than 3,300 stocks.

The reason for the disconnect is because the economic data we are bombarded with is backwards looking. It tells us what happened. Remember, the GDP numbers, for example, report the quarter that ended almost 30 days ago. In fact, most of the other monthly economic data captures what happened in the previous month – with some data reports going back two months. The stock markets, on the other hand, are forward-looking.

How forward does the market look? Well the answer to that depends on who you ask. But generally speaking, the markets look forward at least a couple of quarters, maybe even as much as 18 months.

Going forward, we do know this: we will continue to receive more very negative economic news, especially as data from the second quarter continues to be compiled. We will also continue to receive some very positive economic news (just look at housing data as an example).

All of this data should be viewed with a longer-term perspective.