Saving in an IRA comes with tax benefits that can help you grow your money.

Key takeaways

- Give your money a chance to grow.

- Get tax benefits.

- The earlier you start contributing, the more opportunity you have to build wealth.

It can pay to save in an IRA when you’re trying to accumulate enough money for retirement. There are tax benefits, and your money has a chance to grow. Every little bit helps and you can still put money into an IRA for the 2019 tax year.

Due to the impact of COVID-19, the new date for filing federal income tax returns and for making contributions to your IRA for 2019 is July 15, 2020. It is currently unclear if state filings and payments are affected; taxpayers should consult their advisors for state tax information.

If your employer doesn’t offer a retirement plan—or you’re self-employed—an IRA may make sense.

Here are some reasons to make a contribution now

-

Put your money to work

Eligible taxpayers can contribute up to $6,000 per year, or your taxable compensation for the year (whichever is less), to a traditional or Roth IRA, or $7,000 if they have reached age 50, for both tax years 2019 and 2020 (assuming they have earned income at least equal to their contribution). It’s a significant amount of money—think about how much it could grow over time.

Consider this: If you’re age 25 and invest $6,000, the maximum annual contribution in 2019, that one contribution could grow to $89,847 after 40 years. If you’re age 50 or older, you can contribute $7,000, which could grow to about $19,313 in 15 years.1 (We used a 7% long-term compounded annual hypothetical rate of return and assumed the money stays invested the entire time.)

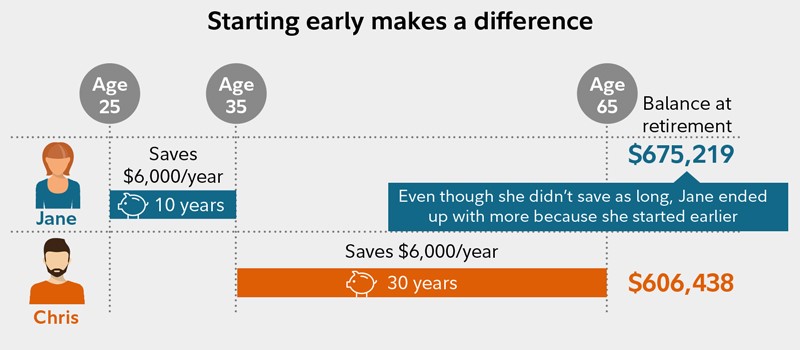

The age you start investing in an IRA matters: It’s never too late, but earlier is better. That’s because time is an important factor when it comes to compound growth. Compounding is what happens when an investment earns a return, and then the gains on the initial investment are reinvested and begin to earn returns of their own. The chart below shows just that. Even if you start saving early and then stop after 10 years, you may still have more money than if you started later and contributed the same amount each year for many more years.

This hypothetical example assumes the following: (1) annual IRA contributions on January 1 of each year for the age ranges shown, (2) annual $6,000 contribution for first year and thereafter, (3) an annual rate of return of 7% and (4) no taxes on any earnings within the IRA. The ending values do not reflect taxes, fees, or inflation. If they did, amounts would be lower. Earnings and pre-tax (deductible) contributions from traditional IRAs are subject to taxes when withdrawn. Earnings distributed from Roth IRAs are income tax-free provided certain requirements are met. IRA distributions before age 59½ may also be subject to a 10% penalty. Systematic investing does not ensure a profit and does not protect against loss in a declining market. This example is for illustrative purposes only and does not represent the performance of any security. Consider your current and anticipated investment horizon when making an investment decision, as the illustration may not reflect this. The assumed rate of return used in this example is not guaranteed. Investments that have potential for a 7% annual rate of return also come with risk of loss.

-

You don’t have to wait until you have the full contribution

The $6,000 (or your compensation limit) IRA contribution limit is a significant sum of money, particularly for young people trying to save for the first time.

The good news is that you don’t have to put the full $6,000 into the account all at once. You can automate your IRA contributions and have money deposited to your IRA weekly, biweekly, or monthly—or on whatever schedule works for you.

Making many small contributions to the account may be easier than making one big one.

It’s important to note that you don’t have to contribute up to the limit each year. Save what you can on a regular basis—even small amounts can make a big difference over time.

-

Get a tax break

IRAs offer some appealing tax advantages. There are 2 types of IRAs, the traditional and the Roth, and they each have distinct tax advantages and eligibility rules.

Contributions to a traditional IRA may be tax-deductible for the year the contribution is made. Your income does not affect how much you can contribute to a traditional IRA—you can always contribute up to the annual limit as long as you have enough earned income to cover the contribution. But the deductibility of that contribution is based on your modified adjusted gross income (MAGI) and the access you and/or your spouse have to an employer plan like a 401(k). If neither you nor your spouse are eligible to participate in a workplace savings plan like a 401(k) or 403(b), then you can deduct the full contribution amount, no matter what your income is. But if one or both of you do have access to one of those types of retirement plans, then deductibility is phased out at higher incomes.2 Earnings on the investments in your account can grow tax-deferred. Taxes are then paid when withdrawals are taken from the account—typically in retirement.

Just remember that you can defer, but not escape, taxes with a traditional IRA: Starting at age 72, required minimum withdrawals become mandatory, and these are taxable (except for the part—if any—of those distributions that consist of nondeductible contributions).3 If you need to withdraw money before age 59½, you may be hit with a 10% penalty unless you qualify for an exception.4

The CARES act temporarily waives required minimum distributions (RMDs) for all types of retirement plans (including IRAs, 401(k)s, 403(b)s, 457(b)s, and inherited IRA plans) for calendar year 2020. This includes the first RMD, which individuals may have delayed from 2019 until April 1, 2020.

On the other hand, you make contributions to a Roth IRA with after-tax money, so there are no tax deductions allowed on your income taxes. Contributions to a Roth IRA are subject to income limits.5 Earnings can grow tax-free, and, in retirement, qualified withdrawals from a Roth IRA are also tax-free. Plus, there are no mandatory withdrawals during the lifetime of the original owner. If you need to take an early withdrawal from a Roth IRA, withdrawals of earnings before age 59½ may be subject to both tax and early withdrawal penalties if withdrawn before the qualifying criteria are met.6

As long as you are eligible, you can contribute to either a traditional or a Roth IRA, or both. However, your total annual contribution amount across all IRAs is still $6,000 (or $7,000 if age 50 or older).

What’s the right choice for you? For many people, the answer comes down to this question: Do you think you’ll be better off paying taxes now or later? If, like many young people, you think your tax rate is lower now than it will be in retirement, a Roth IRA may make sense.

-

You may think you can’t have an IRA, but maybe you can

There are some common myths about IRAs—especially about who can and who can’t contribute.

Myth: I need to have a job to contribute to an IRA.

Reality: Not necessarily. A spouse with no earned income can contribute to a spousal Roth or traditional IRA as long as their spouse has earned income and the couple files a joint tax return. Note, however, that all other IRA limits and rules still apply.

Myth: I have a 401(k) or a 403(b) at work, so I cannot have an IRA.

Reality: You can, with some caveats—as mentioned earlier. For instance, if you or your spouse have access to a retirement plan like a 401(k) or 403(b) at work, your traditional IRA contribution may not be deductible, depending on your modified adjusted gross income (MAGI).2 But you can still make a nondeductible, after-tax contribution and reap the potential rewards of tax-deferred growth within the account. You can contribute to a Roth IRA, whether or not you have contributed to your workplace retirement account, as long as you meet the income eligibility requirements.5

Myth: Children cannot have an IRA.

Reality: An adult can open a custodial Roth IRA (also known as a Roth IRA for Kids) for a child under the age of 18 who has earned income, including earnings from typical kid jobs such as babysitting or mowing lawns, as long as this income is reported to the IRS.7

An adult needs to open and maintain control of the account. When the child reaches the age of majority, which varies by state, the account’s ownership switches from the adult over to them.

Make a contribution

Your situation dictates your choices. If your employer doesn’t offer a retirement plan—or you’re self-employed—an IRA may make sense. But one thing applies to everyone: the power of contributing early. Pick your IRA and get your contribution in and invested as soon as possible to take advantage of the tax-free compounding power of IRAs.

An article from Fidelity Investments

- The hypothetical examples assume the following: one annual $6,000, or $7,000 IRA contribution, as applicable, made on January 1 of the first year; a 7% annual rate of return; and no taxes on any earnings within the IRA. The ending values do not reflect taxes, fees, or inflation. If they did, amounts would be lower. Earnings and pretax (deductible) contributions from a traditional IRA are subject to taxes when withdrawn. Earnings distributed from Roth IRAs are income tax free provided certain requirements are met. IRA distributions before age 59½ may also be subject to a 10% penalty. Systematic investing does not ensure a profit and does not protect against loss in a declining market. Consider your current and anticipated investment horizon when making an investment decision, as the examples may not reflect this. The assumed rate of return used in this example is not guaranteed. Investments that have potential for a 7% annual rate of return also come with risk of loss.

- For a Traditional IRA, for 2019 full deductibility of a contribution is available to active participants whose 2019 Modified Adjusted Gross Income (MAGI) is $103,000 or less (joint) and $64,000 or less (single); partial deductibility for MAGI up to $123,000 (joint) and $74,000 (single). In addition, full deductibility of a contribution is available for working or nonworking spouses of plan participants who are not themselves covered by an employer-sponsored plan whose MAGI is less than $193,000; and partial deductibility for MAGI up to $203,000. For 2020 full deductibility of a contribution is available to active participants whose 2020 Modified Adjusted Gross Income (MAGI) is $104,000 or less (joint) and $65,000 or less (single); partial deductibility for MAGI up to $124,000 (joint) and $75,000 (single). In addition, full deductibility of a contribution is available for working or nonworking spouses of plan participants who are not themselves covered by an employer-sponsored plan whose MAGI is less than $196,000; and partial deductibility for MAGI up to $206,000. If neither you nor your spouse (if any) is a participant in a workplace plan, then your Traditional IRA contribution is always tax deductible, regardless of your income.

- The change in the RMD age requirement from 70½ to 72 only applies to individuals who turn 70½ on or after January 1, 2020. Please speak with your tax advisor regarding the impact of this change on future RMDs.

- You are always able to take money from your IRA. Some withdrawals may be taxable and some may be subject to a 10% early withdrawal penalty. If you are over age 59½, you aren’t subject to a 10% early withdrawal penalty. The CARES Act established some special tax rules for qualifying coronavirus distributions taken in 2020. They must be limited to $100,000 for each individual and would not be subject to the 10% early withdrawal penalty for those under 59½. In addition, the taxes due on the distribution can be spread over 3 years. You may be eligible to take a coronavirus distribution under the CARES Act if:

– You, your spouse, or your dependent is diagnosed with the virus SARS-CoV-2 or with coronavirus disease 2019 (COVID-19)

– You experience adverse financial consequences due to quarantine, furlough, lay off, reduction in work hours, inability to work due to lack of child care, or closing /reduced hours of the business you own or operate, due to the virus or disease.

The qualifying distribution may be repaid to an eligible retirement plan over 3 years.

- For tax year 2019, if you’re single, the ability to contribute to a Roth IRA begins to phase out at MAGI of $122,000 and is completely phased out at $137,000. If you’re married filing jointly, the phaseout range is $193,000 to $203,000. For tax year 2020, if you’re single, the ability to contribute to a Roth IRA begins to phase out at MAGI of $124,000 and is completely phased out at $139,000. If you’re married filing jointly, the phaseout range is $196,000 to $206,000.

- A distribution from a Roth IRA is tax free and penalty free, provided that the five-year aging requirement has been satisfied and at least one of the following conditions is met: you reach age 59½, become disabled, make a qualified first-time home purchase ($10,000 lifetime limit), or die. Required minimum distributions do not apply to the original account owner, although heirs will be subject to them.

- In general, anything that can be legitimately reported as taxable income on a form W-2 is acceptable (although the fact that the income is taxable doesn’t necessarily mean that taxes are paid—the amount could be below the child’s exemption). So money children earn on a paper route is OK, but money given to them by their parents as an allowance probably isn’t. Money earned by a child employed in a family business may be acceptable, but documentation will be required, and the amounts must be reasonable—you wouldn’t be able to claim to have paid your 10-year-old $300 for one hour of sealing envelopes. Always consult a tax expert when in doubt.

Recently enacted legislation made a number of changes to the rules regarding defined contribution, defined benefit and/or individual retirement plans and 529 plans. Information herein may refer to or be based on certain rules in effect prior to this legislation and current rules may differ. As always, before making any decisions about your retirement planning or withdrawals, you should consult with your personal tax advisor.